What Is an Assumable Mortgage?

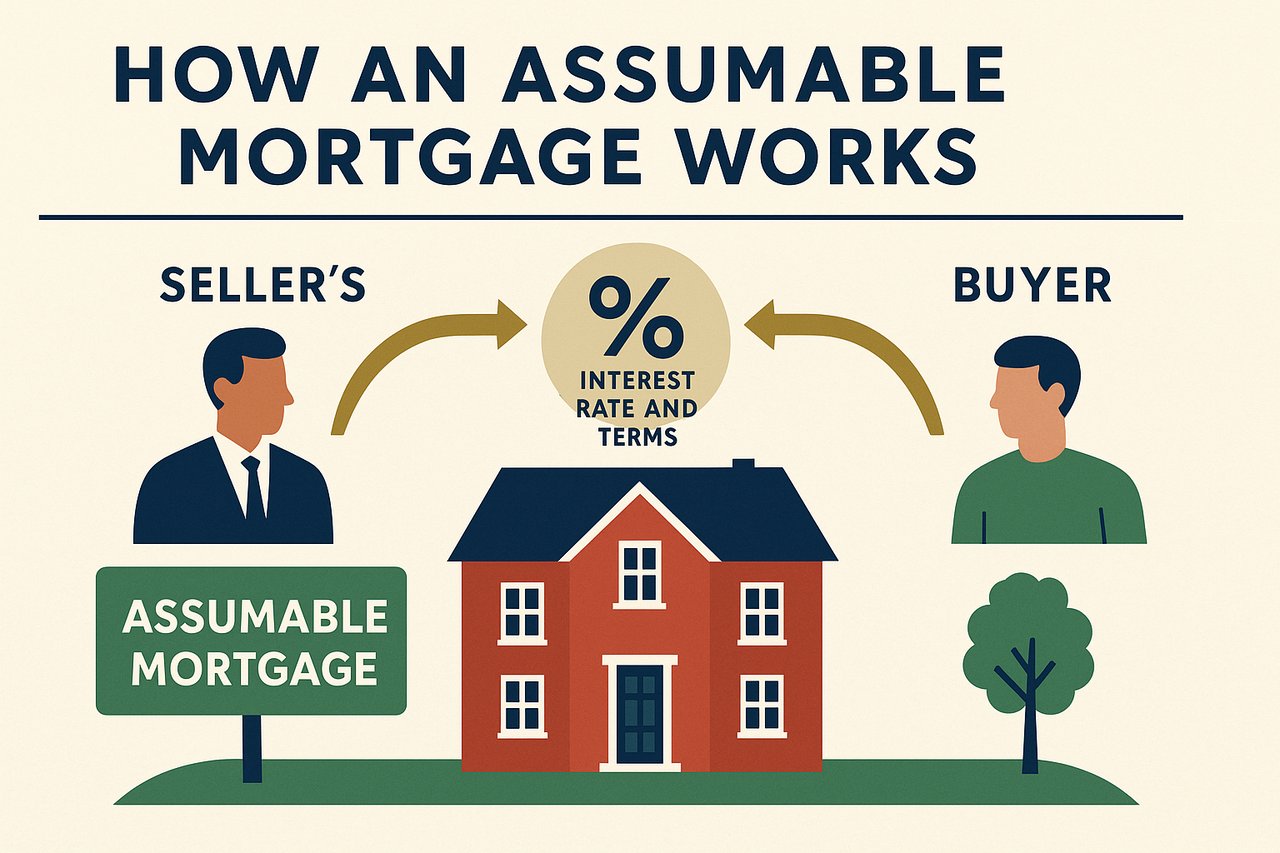

An assumable mortgage allows a homebuyer to take over the seller’s existing loan, including its interest rate, term, and monthly payment. It’s a direct loan transfer from one homeowner to another—no new mortgage required.

That means if a seller locked in a 2.5% or 3% rate during the pandemic, a qualified buyer could take over that same low-rate mortgage today, even as new loan rates hover above 6.5%.

The buyer still needs to be approved by the seller’s lender, who will review credit, income, employment, and debt-to-income ratio. Once approved, the buyer “steps into the seller’s shoes,” taking on the remaining balance and loan terms.

Why Homebuyers Are Paying Attention

The potential savings are eye-catching.

Let’s say a buyer assumes a $500,000 mortgage at 2.5%. The monthly principal and interest payment would be about $1,911.

If that same buyer took out a new mortgage at today’s 6.5% rate, their monthly payment would jump to roughly $2,879.

That’s a difference of $968 per month, or over $116,000 saved over the next ten years.

How the Equity Gap Works

While the savings are real, assumable mortgages come with one major challenge: the equity gap.

This is the difference between the sales price and the remaining loan balance. The buyer must cover that gap—either in cash or with secondary financing (which is often limited).

For example, if the seller’s remaining mortgage balance is $500,000 and the home sells for $800,000, the buyer must bring $300,000 in cash to assume the loan.

For this reason, assumable mortgages typically appeal to buyers with substantial reserves or those selling another property with significant equity.

Which Loans Are Assumable?

Not all mortgages qualify. In fact, most conventional loans cannot be assumed because they include a “due-on-sale” clause, which requires the full loan balance to be repaid when the property transfers ownership.

However, several government-backed loans are assumable, including:

-

FHA loans (Federal Housing Administration)

-

VA loans (Veterans Affairs)

-

USDA loans (U.S. Department of Agriculture)

Buyers who are not veterans can still assume VA loans but may face stricter qualification requirements.

If you’re searching online, look for listings that mention “Assumable Loan” or “FHA/VA Assumption.” A real estate agent familiar with these transactions can help verify if the loan is truly assumable and connect you with the lender to begin the process.

Pros and Cons of Assumable Mortgages

Advantages

-

Lower interest rate: Access rates from years past without refinancing.

-

More buyer appeal for sellers: Homes with assumable loans can stand out in a high-rate environment.

-

Potentially higher sale price: The favorable loan terms can justify a premium.

Disadvantages

-

Large cash requirement: Covering the equity gap can be prohibitive.

-

Limited availability: Only certain loan types qualify.

-

Slower approval process: Lenders often take longer to review assumption requests.

-

Assumption fees: Typically range from $1,000 to $3,000.

Why Assumable Mortgages Are Making a Comeback

Assumable loans are still relatively rare, but they’re becoming more common as rates remain elevated.

According to the Federal Housing Administration, the number of FHA assumable mortgages jumped 127% between 2022 and 2024. That momentum reflects renewed buyer interest in creative financing strategies that can make homeownership more affordable.

For sellers, marketing an assumable loan can create a competitive advantage. For buyers, it can mean locking in a once-in-a-decade opportunity to own a home with a below-market interest rate.

The Bottom Line

Assumable mortgages aren’t for everyone—but in the right circumstances, they can unlock tremendous value.

If you’re buying, they’re worth exploring as part of your financing strategy. If you’re selling and your loan qualifies, highlighting its assumability could help your property stand out and sell faster.

Curious if your loan is assumable, or looking for homes with assumable financing?

I can help you identify options that fit your financial goals and connect you with lenders experienced in the process.